Decarbonization of building heating systems is a huge challenge, due in large part to the sheer scale of the endeavor, but also due to technical challenges and at a very basic level, typical purchase patterns for heating system components. Creating retrofit hybrid heating systems greatly reduces the magnitude of these problems, and while decreasing on-site greenhouse gas (GHG) emissions by 90% or more.

What are hybrid heating systems? Hybrid heating systems are heating systems that consist of more than one heating technology. Sometimes hybrid systems share system components, like a distribution system or emitters, but they don’t have to. Ideally, hybrid heating systems are integrated via one control. A typical hybrid heating system would consist of a legacy boiler or furnace that runs on natural gas, heating oil, or propane, and a heat pump of some sort (e.g. mini-split, air-to-air, etc.). Choice of operation of the heat pump or its fossil fuel alternative can be automated; whichever happens to be optimal at any point in time.

Thinking broadly, hybrid systems are seen in a wide variety of contexts and they are used to solve a problem. In silviculture, grafting branches from one type of apple tree onto the stem of another variety can create a productive and long-lasting hybrid. Hybrid cars provide drivers with better fuel economy and the ability to drive long distances conveniently. Sailboats have hybrid propulsion when they are outfitted with motors to help with navigation in harbors and on windless days. Even drying laundry can loosely be considered hybrid when outdoor drying on sunny days is combined with machine drying on rainy days. Hybrid heating systems have similar appeal as the two main components can complement each other, and actually solve several problems at the same time.

Advantages of Hybrid Heating Systems for Decarbonization

There are actually several good reasons to consider hybrid heating systems for decarbonizing buildings.

1. Efficiency – Hybrid systems can operate much more efficiently than single-source fossil fuel systems, provided a heat pump is one of the components. Higher efficiency leads to reduced GHG emissions.

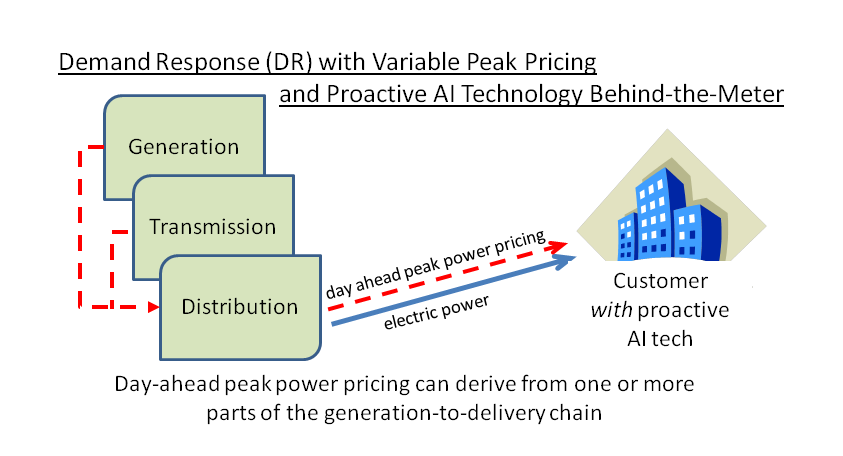

2. Flexibility – Hybrid systems exercise the relative advantages of each heat source, including the ability of a fossil fuel boiler to operate during peak electricity demand periods*, or when the heat pump would be operating at it lowest efficiency.

3. Proactive – Because planning is easier when adding a second heat source, a heat pump can be added to a system at any time of year, which gets around the replacement cycles that center around component failures.

4. Additional weatherization (e.g. insulation, air sealing, etc.), which are highly desirable (even necessary) when heating with a heat pump only, can be accomplished over a longer time frame.

5. Additional system adaptations, such as retrofitting for “low temperature” distribution (i.e. 120F maximum) can be accomplished over a longer time horizon if necessary.

6. Financial benefits – Setting up a hybrid heating system is easier, and less costly than a complete system changeover. Financial incentives for heating retrofits are never unlimited. More GHG emissions can be eliminated by shifting more buildings to hybrid systems, than by shifting half as many buildings to 100% heat pump.

*This is not a huge advantage at this moment, but with increased electrification of heating systems, electricity demand peaks in winter will surpass the level of demand peaks in the summer.

Other Advantages of Hybrid Heating Systems

1. Hybrid systems are redundant. If a boiler or heat pump fails, the building can continue to stay heated.

2. Hybrid systems can heat and cool, so they can replace central a/c and window air conditioners.

3. As long as proper weatherization is in place, hybrid systems can be switched over to single technology/100% heat pump at any time.

More on Flexibility

The ability of a hybrid heating system to be operationally flexible is one of the most important benefits in the race to decarbonize. The reasons why have to do with two things; clean electricity generation and the capacity of the power grid.

Hybrid systems have the ability to reduce peak electricity demand. There is value in having that capability. Much more clean electricity will be generated from solar and wind in the years to come. These are intermittent energy sources. Because of the intermittency, long term battery energy storage systems will be utilized to help provide power when solar and wind aren’t available. Even so, there will be times when supply is limited and demand from electric vehicles and building systems outstrips the supply. So the value of being able to temporarily reduce electricity demand, such as is possible with hybrid systems will grow as more intermittent energy sources feed the grid.

Grid capacity is the other limitation, especially during peak weather events like very cold mornings in winter. As more building heating systems shift from fossil fuels to heat pumps, this will become a bigger issue. Just as described for intermittency issues, buildings with hybrid systems have the ability to temporarily reduce electrical demand by switching to a different energy source, which directly reduces demand on the grid.

More on Financial

Heat pumps operate at very high efficiency, particularly when outside temperatures are not near their winter lows. So building owners (or those paying the energy bills) can save money over combustion-based alternatives that can’t achieve above 100% efficiency.

With regard to asset and installation costs, home and commercial building owners will need some financial assistance to retrofit a system that reduces or eliminates GHG emissions. In what form, and at what level the support takes are worthy of debate but in any case, at any one time, any available support is likely to be limited. Investments in retrofits could be made on hybrid systems, or a smaller number of full changeover heat pump systems where the previous heat source is eliminated. The full changeovers can more than double the initial cost of an add-on heat pump because of the system and weatherization adaptations that are necessary at the start.

Increasing the number hybrid systems will have a greater decarbonization effect than would be the case with fewer transitions to stand alone heat pump systems. This is true at least for the initial period where speed of decarbonization has a high priority.

Summary

Using hybridization of heating system retrofits as a logical step for transitioning buildings with fossil fuel systems will result in the fastest cuts in GHG emissions. Where building owners have the resources to make a full changeover, they should probably do so, as long as they make other changes to reduce demand at the same time. But where external financial incentives are needed, hybrid systems make sense.

New buildings are different. They should be built with no accommodation for fossil fuels, and should be built to minimize the need for heating and cooling through building to passive house standards or similar.

What are the Next Steps?

Clearly hybrid systems can play an important role as a bridge to the future of 100% GHG-free heat. Questions that remain include:

1. what policies and incentives make the most sense to maximize near term GHG reductions?

2. what carrots and sticks make sense in areas like demand charges, energy storage, and variable energy charges?

3. where should subsidies come from and who should benefit?

4. at what level are subsidies or grants needed to achieve GHG reduction goals?

5. what controls are necessary for hybrid systems to operate optimally for GHG reductions?

6. what data should be collected on systems operations to help optimize or balance GHG reductions and end-user costs?

7. should operational data collection be required in return for a grant or other incentive?

8. how are environmental justice and other communities going to be equitably served?

9. how does the workforce need to change to ensure that this will happen?

These and other questions need to be explored, debated and pursued.

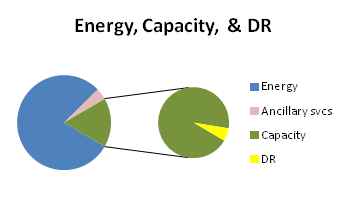

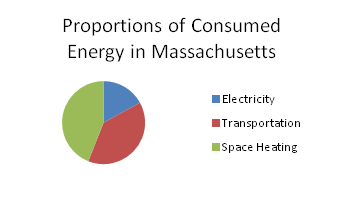

value of DR will continue to grow. The electricity market is a relatively small part of the overall energy mix, but it’s growing strongly. In Massachusetts for example, electricity makes up 17% of consumed energy with the other 83% coming from transport 44%, and thermal 39%. The overall trend is toward electrification of both transportation and space heating, so that the present 17% share of energy is going to move up substantially and relatively quickly. Demand Response has the capability to help facilitate this transition.

value of DR will continue to grow. The electricity market is a relatively small part of the overall energy mix, but it’s growing strongly. In Massachusetts for example, electricity makes up 17% of consumed energy with the other 83% coming from transport 44%, and thermal 39%. The overall trend is toward electrification of both transportation and space heating, so that the present 17% share of energy is going to move up substantially and relatively quickly. Demand Response has the capability to help facilitate this transition.