Reducing energy use in buildings often requires an investment of capital, making an obligation of some sort, or both. As with any investment, there needs to be an acceptable financial return.

Returns are usually quantified in dollars saved. When looked at strictly from a dollars point of view, the investment can be looked at like other investments. The investment might even be compared to alternatives such as repaving a parking lot, expanding a workout area, or hiring more staff. Except it should be easier to quantify the return on the investment in energy reduction. Energy consumption can be easily measured. Things like parking lot improvements and staff may be desirable, but the returns are largely guesswork.

Payback Period

One of the easiest ways to quantify energy reduction return expectations is by estimating a simple payback period. Divide the expected annual savings by the initial cost. If an expected simple payback period is really long, like 15 or 20 years, that investment can be quickly eliminated from contention without spending any more time on it. There are probably alternatives out there that will get a much faster payback.

Limitations to payback period as an investment metric include not quantifying changes in maintenance costs, which are not part of the initial investment. Also not accounted, but very significant are the returns that accrue after the payback period ends. The time value of money is not accounted for.

Discounted Cash Flow Analysis (DCF)

Discounted cash flow accounts for the time value of money, and is therefore a metric that can be used if the quick-and-easy payback period metric passes muster. DCF provides a closer look at the attractiveness of the investment opportunity.

DCF requires using a discount rate. Different discount rates make large impacts on the results of the analysis. Therefore, it’s important to use one that is realistic, and even more important, to be consistent in using the same discount rate for all DCF analyses.

Net Present Value (NPV)

Net Present Value also accounts for the time value of money, as DCF is used to determine NPV. Calculating the NPV results in either a positive number or a negative number. A positive result usually indicates that an investment is worth doing.

Where NPV is less clear is when two different investment alternatives end up with positive NPVs. The larger NPV is usually the best. However, if more initial capital is required to reach that higher NPV, and that capital requirement comes at the expense of other things, such as necessary maintenance, then the answer is not so clear cut.

Internal Rate of Return (IRR)

The internal rate of return is another useful metric. It shows the discount rate where the NPV of cash flows = zero (assuming NPV is positive). The IRR is useful for determining if an investment is worthwhile. If the IRR is higher than the cost of capital, and there is confidence in the assumptions made to determine the IRR, then the investment is probably worthwhile.

Valuation Effects

Another consideration for energy cost reduction is how the reduction in costs effects valuation. A change to energy assets that creates a lasting and meaningful energy cost reduction most definitely will increase the value of the property or business. Of course, to be true, the scale of energy use reduction must have a material affect on the cost structure.

More details about the subject of how energy costs cuts affect valuation is available in this blog post.

Other Financial Considerations

In the world of energy efficiency, there are often additional factors to consider. Some of these factors include:

- No money down loans

- Low interest loans

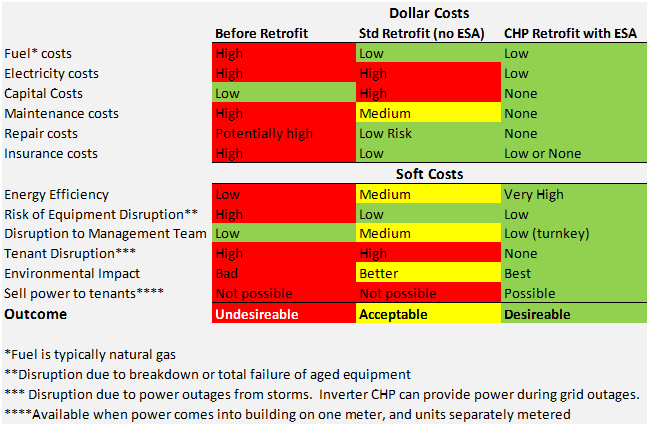

- Energy services agreements (ESAs)

- Tax credits

- Tax deductions

- Accelerated depreciation

- Grants

- Discounted fuel

- Discounted power

- Tradeable credits, and more.

CIMI Energy Can Help

CIMI Energy can perform these financial analyses and write up reports that help you to prioritize where to focus.

Beyond the financial aspects of these investments, there are environmental and sustainability considerations. CIMI Energy can help with this also. If so desired, these considerations can be considered within the reports.