Demand response (DR) exists to provide value to electric utilities and their customers. In any of its manifestations, the effect of DR is to temporarily reduce end-user demand on utility supply resources.

Demand response (DR) currently exists for these purposes:

- to limit peak demand during temporary periods of peak heating or cooling

- to offset supply disruptions, transmission outages, or other capacity constraints

- to adapt energy systems to the intermittency of supply from solar and wind energy

DR experienced strong growth over the past 10 years. DR will grow strongly in this new decade as well, although the factors leading to growth must change. The obstacles that stand in the way of continuing with the established growth phase relate to ability to scale, regulations, and cost efficiency.

DR in the 2010s

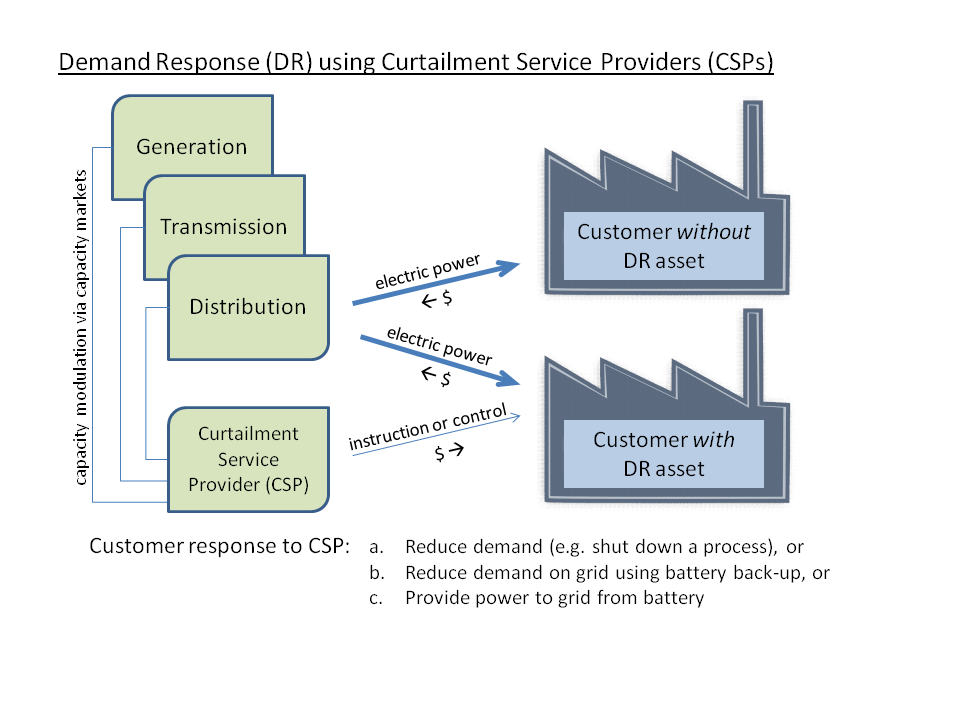

Demand response in the 2010s was almost exclusively managed from the supply side. Strong growth in DR was facilitated mainly by Curtailment Service Providers (CSPs) that serve the power capacity markets. Growth was also made possible by advancements in controls technology, energy storage such as customer-sited batteries, and various government and utility incentives. The CSPs serve the capacity markets. Capacity markets ensure that load serving entities (LSEs, e.g. electricity transmission and distribution) commit to providing adequate supply, particularly peak supply, to balance demand throughout the year. As part of the capacity market, DR functions as if it were an LSE, although technically it is not.

On the demand side, the most typical DR placement was, and still is with industrial/manufacturing consumers of electrical power, which represent 50% of the market or more. By its very nature, industry is well suited for DR. Industry uses electricity in its processes, and when those processes aren’t needed 100% of the time, it’s often possible to shift power consuming processes to different times of day, or even different days altogether. Large batteries or other forms of back-up power can also be used if the savings from DR are high enough to cover the costs.

Limitations of the Status Quo

As noted previously, DR capability must be available to curtail load year round in order to be accepted in the capacity market. This is a regulatory requirement. This requirement for year round curtailment capability is only possible when the DR capability is a subset of Capacity Performance (CP). Today, 95% of DR revenue comes from CP. However, being reliant on capacity markets is problematic.

Scale Issues

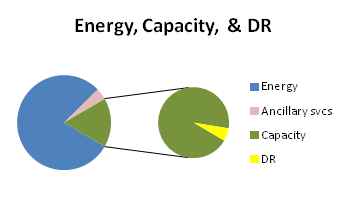

According to PJM, power capacity accounts for only about 15% of the overall spend for power. If the power market (generation, transmission, and distribution) is a whole pie, the power capacity market is one slice of that pie, and DR is about 5% of that slice of pie, or just one bite of the whole pie. In other words, despite its growth, DR is still a relatively small part of the power market. If it is going to continue to scale, it will need to move beyond the capacity market.

Economic Efficiency

Another issue with DR being relegated to the capacity market is that the capacity market is not a market optimized for economic efficiency. The main objective of CP is to ensure sufficient capacity is available to meet demand at all times. For DR, this leads to a side effect that’s known as the double payment issue. Currently, when owners of the DR asset reduce demand, they not only reduce energy costs, but they also get paid to do so. In other words, the DR asset owner gets rewarded twice for the same action. This double payment effect can lead to gaming of the system for profit. Alternatively, if sought changes in demand were resulting from demand pricing alone, then the double payment issue would be avoided. As a result, economic efficiency would rise.

Regulatory Considerations

The FERC has regulatory oversight over the RTOs. The regional transmission organizations (e.g. PJM, ISO-NE) administer forward capacity markets. In Q4 of 2019, FERC weighed in on PJM and the capacity markets serving it. FERC placed burdens on new DR installations which effectively render them uneconomic (see 169 FERC ¶ 61,239).

Whether the new FERC regulations adhere long term remains an open question. Either way, these regulations demonstrate the uncertainty that is inherent in government regulatory authority. The best way to avoid regulatory involvement is to focus on markets that run themselves without the need for government involvement between parties.

DR in the 2020s and beyond

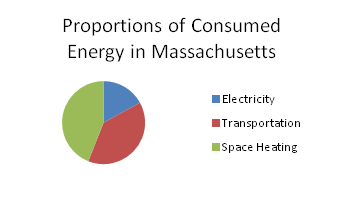

The value of DR will continue to grow. The electricity market is a relatively small part of the overall energy mix, but it’s growing strongly. In Massachusetts for example, electricity makes up 17% of consumed energy with the other 83% coming from transport 44%, and thermal 39%. The overall trend is toward electrification of both transportation and space heating, so that the present 17% share of energy is going to move up substantially and relatively quickly. Demand Response has the capability to help facilitate this transition.

value of DR will continue to grow. The electricity market is a relatively small part of the overall energy mix, but it’s growing strongly. In Massachusetts for example, electricity makes up 17% of consumed energy with the other 83% coming from transport 44%, and thermal 39%. The overall trend is toward electrification of both transportation and space heating, so that the present 17% share of energy is going to move up substantially and relatively quickly. Demand Response has the capability to help facilitate this transition.

Because of these strong trends, opportunities for growth in DR are best in new market segments, using different strategies and technologies. Take for example the fast growing trend in transportation powered by electricity. Demand for electrically-powered transportation, particularly cars and trucks, is expected to grow strongly for decades to come. The growing demand for electrical power in transportation will place transportation alongside the other large user segments of electrical power: industrial, commercial and housing.

The housing sector, specifically in heating, cooling and domestic hot water (DHW), is another growing area for electricity consumption. The growth is coming from more heat pumps being installed. Technologically speaking, heat pumps have progressed significantly over the past decade. Because they perform very efficiently, and they have the ability to be used for both heating and cooling, they are already growing strongly in supplemental retrofit situations. They are also being used more and more in new construction as well, and may well completely displace oil and gas within a couple of decades.

The market for electricity is dependent on its infrastructure. As the trend toward electrification gains momentum, there will be more demands made on the grid. It’s hard and expensive to build new transmission assets in built-up areas. Both efficiency and DR will make important contributions to meeting these new demands.

Moving Decision-making from Supply Side to Demand Side

Because demands on the electrical grid are becoming greater, especially during peak events, growth in DR is desperately needed. Some of the growth can be supported by the capacity markets. But as capacity markets are small relative to the expected increase in demand, there is a much larger opportunity for growth outside of the capacity markets.

Growth can come from any other part of the supply chain, such as generation, and LSEs (transmission and distribution), wherever there is some value either in lowering peak demand or in shifting demand away from peak hours. Value can be perceived by one or any combination of participants in the supply chain. The value from reducing peak demand can be temporary, such as just a few hours. And it can be either one-off or recurring, such as, for example any day where temperatures exceed 85°F, or fall below 20°F.

Achieving Economic Efficiency with DR

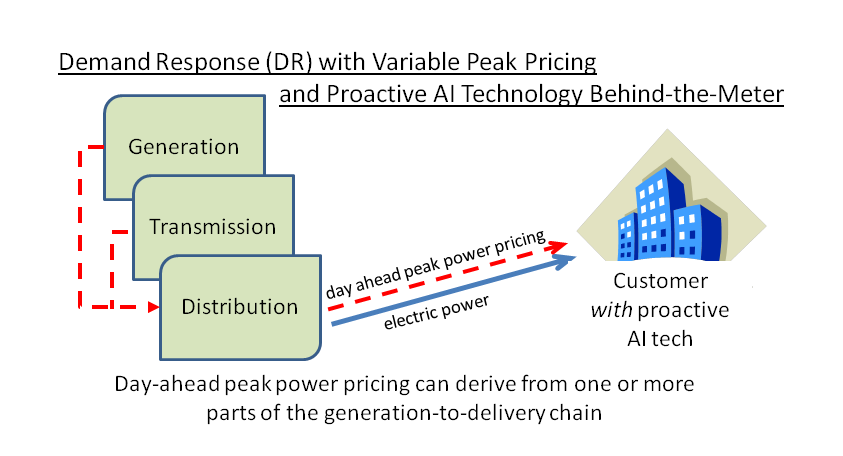

In the coming decade, the financial catalysts for growth need to change. The opportunity for growth will shift from the capacity market to the energy market; the energy market share of the pie is much bigger, and there’s more latent value to be realized. Suppliers can affect demand by varying the price. There’s an opportunity to improve economic efficiency by letting suppliers use market forces to determine peak demand pricing on a day ahead basis.

Demand Side Management (DSM) offers potential for shifting demand away from peaks. With pricing signals, demand can be proactively reduced or shifted, depending on the goals of the entity making the price.

Keys to successful variable demand pricing includes interval metering, day ahead pricing, and technology that uses price signals to modulate demand. Also important is finding how elastic the demand is for classes of energy consumers. As day ahead demand pricing will be an important component of growth in DR in this decade, and because there is a learning curve to using it, it’s important to start planning and using it as soon as possible.

Be sure to follow if you’re interested in this subject as I will be following up with more on the future of DR growth for utilities in the weeks to come.

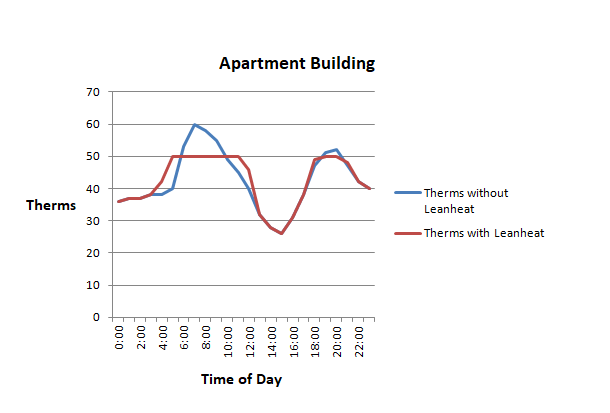

The example shows the exact same consumption over the 24 hour period. The only difference between the two is that the red line is flatter, spreading out the demand, and maxing out at 50 therms/hour, a 17% reduction from the 60 therm/hour peak.

The example shows the exact same consumption over the 24 hour period. The only difference between the two is that the red line is flatter, spreading out the demand, and maxing out at 50 therms/hour, a 17% reduction from the 60 therm/hour peak.